WHY ARE YOU STILL ASKING ME ABOUT BBA AND BAI AL INAH?

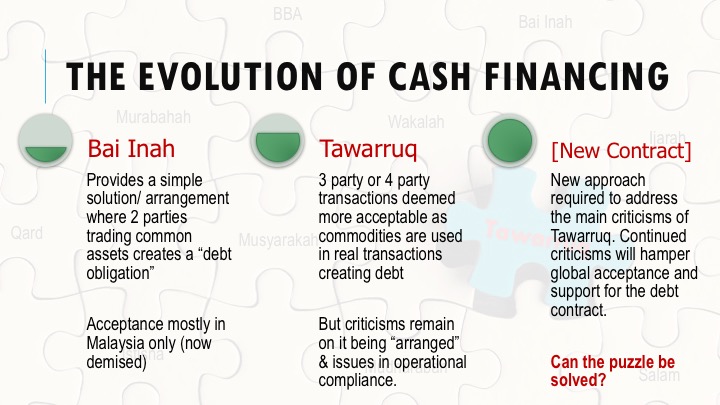

It remains a mystery when people ask me why Malaysia continues to offer Bai Bithaman Ajil (BBA) and Bai Al Inah products, as according to them, these structures are based on elements of Hilah (trickery). It is a mystery because starting from 2012/2013 period, the instructions on Interconditionality issued by BNM to Islamic Financial Institutions requires that the provisions of “mandatory buy-back” must not appear in financing contracts such as Bai Inah and BBA. Because of this, Malaysian Islamic Banks have slowly weaned itself from such products and have since moved to other Islamic contracts.

It remains a mystery when people ask me why Malaysia continues to offer Bai Bithaman Ajil (BBA) and Bai Al Inah products, as according to them, these structures are based on elements of Hilah (trickery). It is a mystery because starting from 2012/2013 period, the instructions on Interconditionality issued by BNM to Islamic Financial Institutions requires that the provisions of “mandatory buy-back” must not appear in financing contracts such as Bai Inah and BBA. Because of this, Malaysian Islamic Banks have slowly weaned itself from such products and have since moved to other Islamic contracts.

WE ARE STILL READING OLD BOOKS AND ARTICLES

In general, I still find that some learning institutions are incorrectly teaching students that the contracts are still alive and well in the Malaysian market. The text books used are still ones that predates 2011 and really, this is a disservice to students. When they come for interviews with our bank, it does not give the students any advantage or good impression as the syllabus remains outdated. Many do not know about the Policy Documents issued by Bank Negara Malaysia or the contracts covered by the policy documents. This really should be covered in a learning module as the latest requirements are captured in these documents. It is a good reference read, but it seems only practitioners and Shariah scholars are aware of these documents.

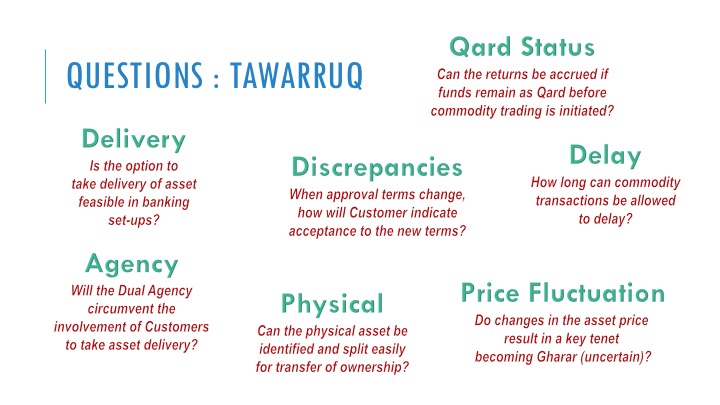

This is true as my last few interns also impressed the same. Tawarruq structures sounds alien to some of them, as their teachers prefer to teach BBA and Bai Inah to unlock its controversies as points for discussion. Let us be clear that most banks NO LONGER offer Bai Inah or BBA, and those which does, offer it as a continuation for a legacy arrangement or due to certain unavailable scenarios, such as fresh new documentations are not obtained for Tawarruq arrangement (such as Wakalah to buy commodities). It is no longer offered as a product to the public and this is evidenced from the Banks website where the structures can no longer be found. And most of the time if used, this is a temporary fix allowed until the deal reaches expiry or the Tawarruq appointments are obtained.

And with Tawarruq arrangements now being ably supported by good infrastructure such as Bursa Suq As Sila trading platform and other commodity brokers worldwide, there is no issue of Darurah (emergency) to justify the continued usage of Bai Al Inah or BBA.

SO, WHERE HAVE WE GONE TO SINCE 2011?

In short, we have moved to the following contracts:

- Bai Bithaman Ajil (BBA) – Usually BBA is used for purchasing of properties (Home financing or Commercial properties financing), or sometimes for trade financing products. These usage is now done under the Tawarruq arrangement (using Commodity Murabahah) where the proceeds from the sale of Commodities is used to settle the purchases of houses or commercial properties. Alternatively, Musyarakah Mutanaqisah arrangement (Diminishing Partnership) is also used by many banks where houses or properties are purchased by the Bank and leased out to the customer, who then pays rental and gradually purchases the shares of the house and properties over time. So now, BBA has been replaced with Islamic arrangements of Tawarruq or Musyarakah Mutanaqisah. Other Islamic contracts has also been known to support some elements of BBA, such as Istisna’a (property construction), Murabahah (good sale at profit) or Ijarah / Ijarah Mausufah fi Dhimmah (forward lease).

- Bai Al Inah – Usually Bai Inah is deployed for Personal Financing or Working Capital Financing and even Islamic Credit Cards. Again, Tawarruq arrangements has generally replaced these usage with the end result of providing cash. On a smaller note, the contract of Ujrah (Services) is also deployed to support some requirements of personal financing (where purchase of goods and services are required) and Islamic Credit Cards. So now, Bai Al Inah has now been replaced by Tawarruq arrangements or Ujrah contract to meet the cash and working capital requirements.

The final controversial contract that Malaysia currently deploy is the Bay Ad Dayn (Discounted Sale of Debt), which serves a specific purpose in trade financing products. Eventually a common ground must be found to make this contract more globally accepted, or replaced with a better solution.

UPDATE YOUR STUDY NOTES, PLEASE

The main challenge nowadays is to innovate further by improving what we have. Criticisms are good, especially on the old structures. But we practitioners do hope the learning academia afford us a bit more confidence and trust, especially these criticisms and consequent issues are not “unknown” to us, since we lived and breathed in its controversies many years ago. The comments made in recent times are something we had encountered and resolved 10 years ago. We enhance and evolve, and it will be good to see new students coming into the market armed with the latest updates of what is happening and let’s move forward.

It is now 2019. Do not get stuck in the muddy past. These contracts have gone into the history books. We have so much to do in the future arena.