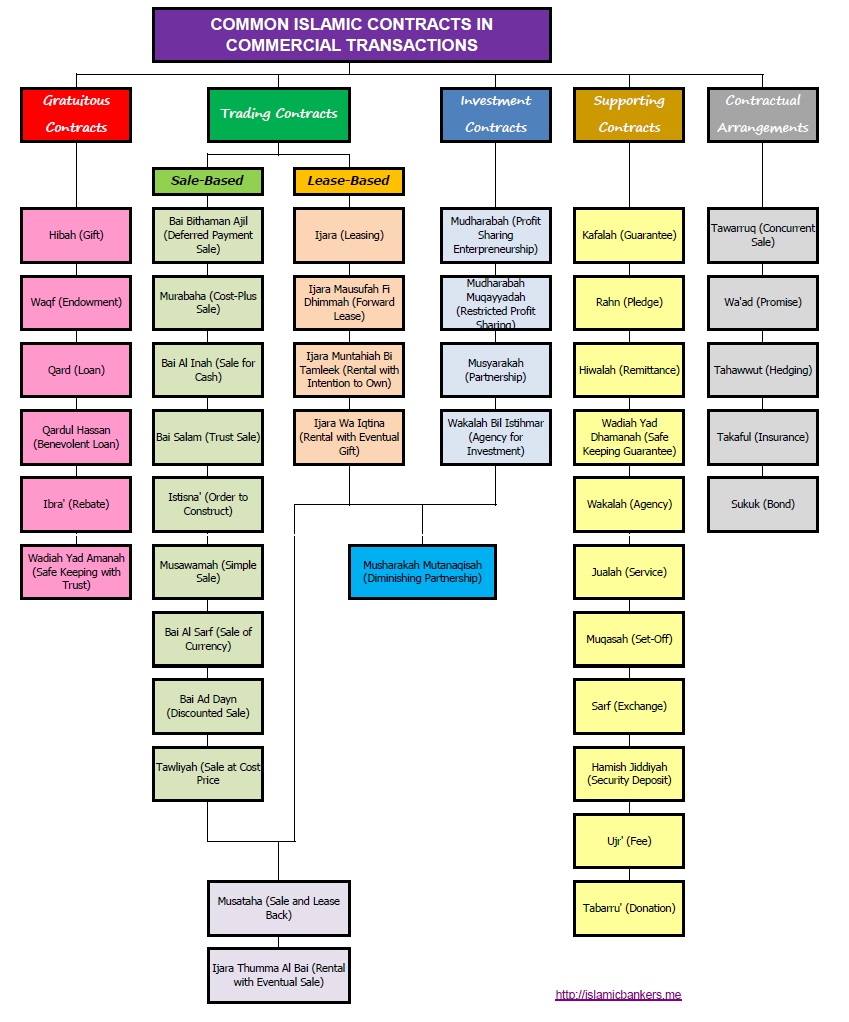

It is reaching the end of the year and I thought it will be good to have a quick look on how many Islamic Banking contracts that we have in and around the industry. Granted, I might miss some of the contracts as there are many banks offering hybrids nowadays. I do apologise for such shortfall, and will endeavour to update this chart as often as possible, should there be some interesting and new contracts being introduced in the Islamic Banking industry.

In general, common Islamic Banking contracts can be segregated into a few categories:

- Gratuitous Contracts

These types of contracts are typically unilateral in nature where the contracts do not require mutual consent to be applied. It is just a one-way arrangement where one party provides a product or service based on mandates or scope of work and is at discretion to vary the terms without requiring the other party to specifically accept the changes. For example, the Hibah contract (Gift). One party provides the gift, and the other party receives the gift. It should be on a unilateral / discretionary basis by it not being “promissory”.

Another example is the contract of Qard (Loan). One party lends money to the other party, and the other party (borrower) undertakes to pay back the loan (original amount) when required by the lending party, without any expectation of additional return. But the other party (borrower) can pay more than the original amount (by way of Gift) but is not obliged to, and such additional gift do not require the borrower to obtain “consent” from the lender to be given. It is simply the payment of the loan, and any other gift (which is not obligatory). Such “gifts” avoid the definition of Riba’ by being not promissory.

Under gratuitous contracts, the Aqad is not greatly necessary (it being unilateral) but it will be ideal for all parties if an Aqad can be concluded upon.

- Trading Contracts

Trading or transactional contracts are debt-based contracts. Very similar in nature and intention to a conventional loan, but requires specific Islamic contract to be perfectly executed to avoid riba’. Such contracts greatly involves the participation of 2 parties (sometimes 3 or multiple parties) and there is a defined Aqad executed to finalised the terms and conditions to the contract. These terms are to be defined and agreed upon within the Ijab/Qabul period for all parties to accept. Once accepted, any proposed further changes captured in the Aqad must be accepted by all parties by mutual consent.

A common example will be a Murabaha financing transaction, where the terms and conditions are agreed up-front in a bilateral agreement. A purchase price is discussed, together with the profit amount, selling price and the settlement tenure. Ownership of the asset (used as an underlying asset for the Murabaha) is also moved between the parties, and transactional sequence is observed. Any changes that is proposed outside the Aqad majlis will require approval and consent by all parties.

A Leasing contract is also deemed a bilateral contract although the owner of the asset has the right to unilaterally increase or revise the rental amount of the asset under hire / rental, the person who lease that asset will also have a right to remain in or exit out of the leasing arrangement, thus making it bilateral (where there is also a material change in the terms and conditions.

The perfection of Aqad holds great importance to Transactional Contracts to ensure the validity of the transactions.

- Investment Contracts

These types of contracts deals more on equity and corresponding returns in the subject matter. It follows the concept of investment where such equity-based structures takes on the risks of the investments, and concentrate on the concept of entrepreneurship and risk-sharing. In such contracts, where there is an element of trust, bilateral arrangements are strictly adhered to. Changes to the terms and conditions requires explicit consent especially from the party that is in a disadvantageous position.

The most popular of these contracts is the Mudharabah, which is used in many depository products. However, although this is technically a deposit, these deposits must be utilised or deployed into economic transaction for the purpose of generating a return on the capital i.e. in this case, the Mudharabah deposit. Once profit is recognised (if ever…) then the profit must be distributed to the customers based on the agreed Mudharabah profit sharing ratios. The Bank, usually acting as a Mudharib (fund manager / entrepreneur) , will behave as a pure entrepreneur with the customer (as Rab Ul Mal), acting as the fund provider with the possibility that the investments is not up-to-market returns which can result in both loss in profit and loss of principal (principal not guaranteed).

Another example. Under a Musharakah structure, there is even more defined roles that the all parties must take and agree under a bilateral arrangement. With Musharakah, each party will be required to contribute equity (or capital) and even contribute expertise into the partnership venture to ensure profit can be made. All terms and conditions are captured as part of the important Aqad. Any profits declared will be shared according to equity ratio or agreed profit sharing ratio, and any losses shall also be shared amongst partners, usually based on equity ratio or equity contribution.

- Supporting Contracts

Supporting contracts are often important because they act to complete many aspects of services, products and banking. Many supporting contracts are created to cater mostly for specific situation and most of it requires proper Aqad as well. Such contracts are also considered a facility to provide specific outcomes for the customer. It also falls into a bilateral arrangement.

Popular contracts include the contract of Kafalah (guarantee) where a person can enter into a Kafalah to secure a financing facility by providing a letter of guarantee. Other contracts include Rahn (mortgage or pawn broking) that has specific terms to the arrangements, Hamish Jiddiyyah (security deposit) or even Wakalah (Agency for services)

- Contractual Arrangements

Contractual Arrangement are not necessarily contracts on its own, but can be construed as a combination of contracts to achieve a certain objective. The arrangement itself is not legally binding, but what is inside those arrangements are usually standalone valid Islamic Banking contracts.

Take for example the contractual arrangement of Tawarruq. Inside a Tawarruq arrangement, it consists of several standalone Islamic Banking contracts. Firstly there is the contract of Wakalah (Agency) to purchase the commodities on behalf of the transacting party. Secondly, there is the contract of Commodity Murabahah where the commodities purchased will be sold at a Sale Price to the purchasing party. Once the Commodity ownership is transferred into the purchasing party, the purchasing party can make an offer to another party as a Musawamah (simple sale) to obtain the desired cash.

Other contractual arrangement is the arrangement for Wa’ad (Promise) usually used for FX transactions. A Wa’ad itself is not binding, but it can be enforced upon certain events where eventually an exchange can be made (Sarf) or even a Commodity Murabahah is executed to deliver certain obligations.

Again, these are not exhaustive list of contracts, and can easily be expanded in a short period of time. Innovations are done everyday, and it will be a matter of time until critical mass will push a contract to the forefront. I hope to keep updating this list more in the coming years.

Wallahualam.