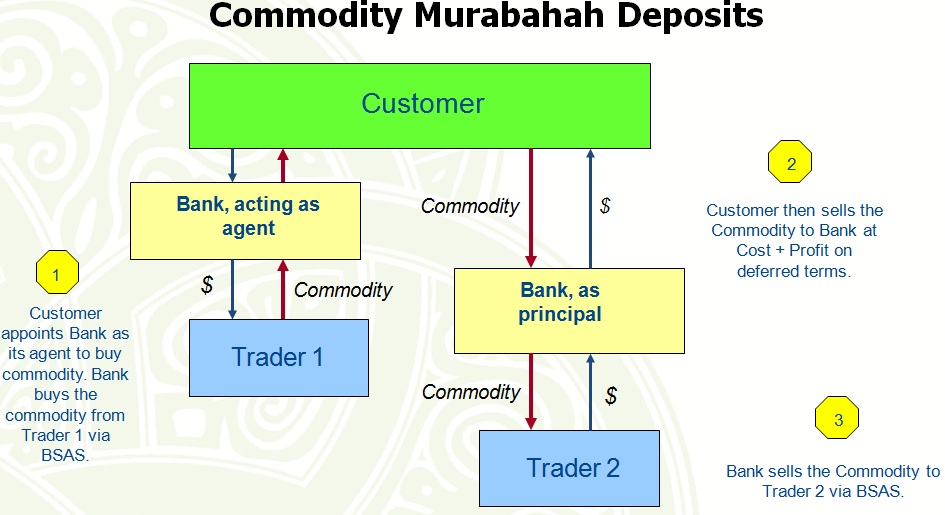

A few days ago, several Banks in Malaysia officially made available Deposit products based on Commodity Murabaha transactions.

Looks like Commodity Murabaha (CM), or in another variation is called “Tawarruq” has now expanded its domain from Financing-based to Deposit-based products. More and more banks will have to rely on this structure on both sides of the balance sheet. Bai-Inah based portfolio used to consist of nearly 80% of the overall financing portfolio of some banks; now with the push for Commodity Murabaha structures in financing to avoid interconditionality issues in Bai-Inah, it is expected that Commodity Murabaha financing to eventually replace the Bai-Inah portfolio.

Now with the introduction of CM for Deposits, the popularity of commodities will take a sharp rise! Bursa Malaysia will have their hands busy supplying the industry with commodities to support the underlying transactions. Islamic bankers will also have their hands full buying and selling commodities between the bourse and the customers, either as buying agents or principal purchasers!

I am not sure whether this is necessarily a good thing.

The industry will now shift from having a Bai-Inah-heavy portfolio into a Commodity-Murabaha-heavy portfolio. Concentration risks towards one Islamic contract will grow, and the question is that whether Banks will take the time to develop other contracts into viable propositions instead of just building the CM infrastructure. Do bear in mind that a lot of infrastructural work needs to be done to ensure CM remains the flagship contract for years to come.

The specific risks that Banks faced when offering CM products are manifold; shortage of commodities, delays in transactions, wrong sequencing of purchase and sale of commodity, errors in commodity prices and description, delivery of commodities issues, ownership issues and ownership evidencing. All these requirements needs to be watertight to ensure income from these CM transactions don’t just go to charity. Whenever there is an Asset involved in the transaction, all the factors need to come together to ensure Sharia compliance.

And the way we are going, it seems that CM will probably have 80% of the financing pie and 70% of the deposits pie in a typical Islamic Bank’s balance sheet in 3-5 years time. With IFSA deadlines on June 2015, this ratio could come sooner rather than later.

Will the development of other contracts be further left behind since the shift now is on CM? Maybe, historically Malaysian Banks follows the “Urf Tijari” route of following what the other bank is doing. We have seen this when Bai Bithaman Ajil (BBA) was introduced; nothing else was developed in the market but BBA. It was the same with Bai Inah.

But there is other opportunities for development of other Islamic contracts, although I don’t imagine this is the case for Malaysia while we busy ourself becoming commodity traders. Oman, on the other hand, has rejected tawarruq totally, focusing on other contracts such as Ijara and Musyaraka. This is a good development, as no countries has seriously looked at developing complex, high-risk structures. Maybe once the thinking to shift to understand the transactional and Sharia risks of the new products is made, perhaps the market can warm up to the idea that Sharia compliant banking can be a different way of banking.