The following is what I understood from the various Exposure Drafts issued by BNM on 9 December 2013. Of the 7 exposure drafts that we received, I have earlier summarised the Wadiah Exposure Draft, and I will ignore the Bai-Inah Exposure Draft as we are no longer subscribing to the Bai Inah structure at the workplace.

Please find the remaining Exposure Draft review for your understanding.

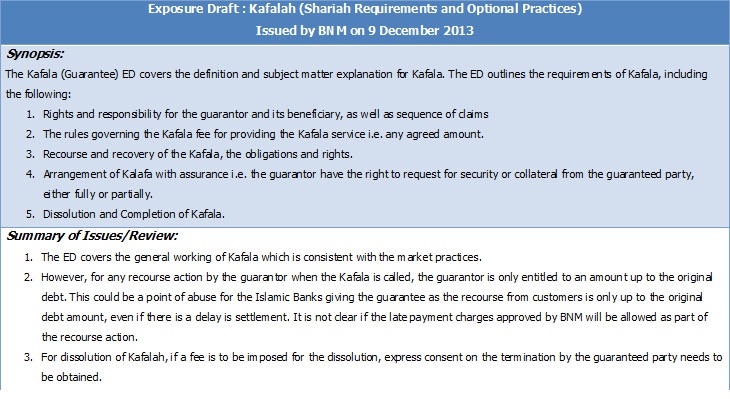

2013 ED – Kafalah – One of the key issues for a Kafala (Guarantee) contract is the charging of fees for providing the guarantee services. The main issue has always been the quantum of fees charged, either in percentage of the financing or via a fixed charge for all financing amount. The justification of this charge is always tricky, because technically the fee should not be imposed if there is no call for the guarantee (in cases of no default). The guarantee will only materialise if the customer defaults, that’s when the work happens to justify any fees. Issuing a piece of paper at the start of the relationship to guarantee the amount does not amount to too much work, and there no funds disbursed to any parties (unfunded). To justify the charging of any fees based on percentage instead of actual work, especially for huge amounts of financing guarantee, can be problematic to justify in the eyes of Sharia.

2013 ED – Wa’d – At one point of time, Wa’ad (Promise) seems to be the answer to many structures, where a promise is given without any requirement to transact before a specific event. The terms therefore can be negotiated and re-negotiated without the need to strictly specify the terms of the transaction and re-signing of documents. This gives a lot of leeway for deals to happen.However, at the end of the day, Wa’ad remains as only a promise, legally distanced from a contract or an agreement. Enforcement at the courts are therefore without full confirmation of all the terms, and makes for a loose structure and potential disputes. This flexibility and enforceability remains one of the key risks to a Wa’ad contract, which is why until today Wa’ad is generally transacted between known parties i.e. between established and trusted Financial Institutions.

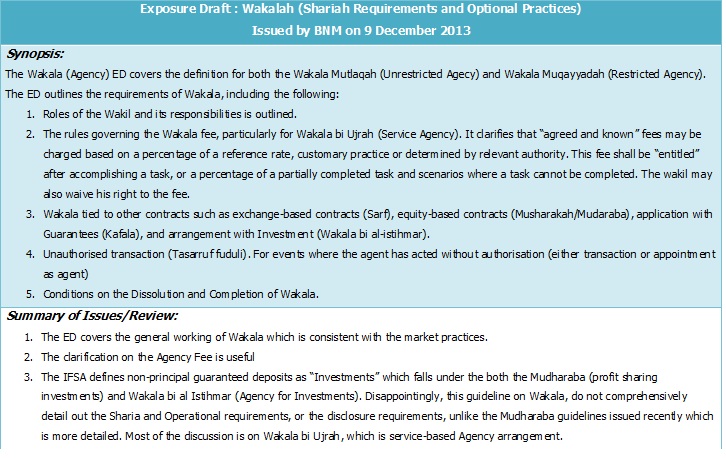

2013 ED – Wakalah – Wakala (Agency) will remain an integral contract for Islamic Banking as it validates a lot of action that can be done by the Bank, in order to remain efficient. In general, Banks hold a lot of expertise in various fields, such as investments, financing, leasing and trading; something a normal customer may not want to be involved in on a daily basis. An Agency arrangement conveniently provides for this. Anything that improves the efficiency by leveraging on the Bank’s expertise and infrastructure, can be arranged via Agency. However, the way we practice it usually is transparent to the customer. In practice, Agency Fees are the right of the Agent, and the waiver of such fees, although allowed, is sometime seen as not adhering to the spirit of Agency and entrepreneurship. You do the work as an Agent, but don’t earn any fees as it is waived. In real life, this does not happen as whenever a work is completed, you should earn something.

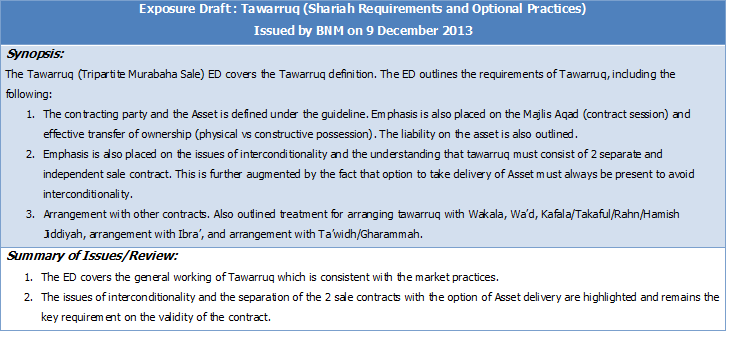

2013 ED – Tawarruq – As Tawarruq (Three-party Murabaha Sale) becomes more prominent in the Malaysian market, I was surprised that the ED was not more comprehensive than this. There are sequencing issues not addressed but more importantly, there is a lack of illustration on what is defined as Tawarruq. Is there any difference between a Tawarruq and Commodity Murabaha, which essentially is a 4 party transaction? The issue of interconditionality is adequately addressed in the ED but I would love to have seen more details related to products, such as for Islamic Credit Cards and Revolving Credit with a rebate structure (Ibra’) based on a floating rate financing. It mentions that the discount can be given based on certain benchmark agreed by the contracting parties. This opens the clause to various interpretation as it is without real detail.

I will look at the Hibah (Gift) ED but essentially, it is related to the Wadiah ED. Most of what’s covered under the Hibah ED is relevant to the Wadiah product, such as the discretionary Hibah issue and the giving of Hibah becoming a business practice (Urf Tijari) which can be construed as Riba (Usury). Wait for the posting.

Thank you for reading, hope everyone have an enjoyable holiday period ahead. Wasalam.