SOURCES OF FUNDS

Islamic banks rely on the following sources of funds:

-

Capital & Equity;

-

Transaction deposits that are risk free and yield no return; and

-

Investment deposits that carry the risks of capital loss for the promise of variable returns.

Capital & Equity

-

Capital is the amount injected into the Islamic bank during the setting-up stages i.e. the paid-up capital of the Islamic bank.

-

Equity is usually the retained earning of the Islamic bank that accumulated during its operational period.

Transaction Deposits

-

Current accounts

Current accounts are based on the principle of Wadiah, whereby the depositors are guaranteed repayment of their funds. At the same time, the depositor does not receive remuneration for depositing funds in a current account, because the guaranteed funds will not be used for PLS ventures. Rather, the funds accumulating in these accounts can only be used to balance the liquidity needs of the bank and for short-term transactions on the bank’s responsibility.

-

Savings accounts

Savings accounts also operate under the Wadiah principle. Savings accounts differ from current deposits in that they earn the depositors income: depending upon financial results, the Islamic bank may decide to pay a premium, hiba, at its discretion, to the holders of savings accounts.

Investment Deposits

-

Investment accounts

An investment account operates under the Mudaraba al-mutlaqa principle, in which the Mudarib (active partner) must have absolute freedom in the management of the investment of the subscribed capital. The conditions of this account differ from those of the savings accounts by virtue of:

1. a higher fixed minimum amount,

2. a longer duration of deposits, and

3. most importantly, the depositor may lose some of or all his funds in the event of the bank making losses.

-

Special investment accounts

Special investment accounts also operate under the Mudaraba principle, and usually are directed towards larger investors and institutions. The difference between these accounts and the investment account is that the special investment account is related to a specified project, and the investor has the choice to invest directly in a preferred project carried out by the bank.

UTILISATION OF FUNDS

To generate revenue, Islamic banks utilized the funds by giving out financing facilities. The financing facilities are done based on the Islamic concepts accepted by the Islamic bank Shariah Council / Committee.

The concepts usually applied by the Islamic bank are as follows.

- Murabaha (cost plus / mark up)

This is the most commonly used mode of financing device. In a Murabaha transactions, the bank finances the purchase of a good or assets by buying it on behalf of its client and adding a mark-up before reselling it to the client on a cost-plus basis profit contract.

-

Bai’ muajjal (deferred payment)

Islamic banks have also been resorting to purchase and resale of properties on a deferred payment basis. It is considered lawful in Fiqh (jurisprudence) to charge a higher price for a good if payments are to be made at a later date. According to Fiqh this does not amount to charging interest, since it is not a lending transaction but a trading one.

-

Bai’ salam (prepaid purchase)

This method is really the opposite of the Murabaha. There the bank gives the commodity first, and receives the money later. Here the bank pays the money first and receives the commodity later, and is normally used to finance agricultural products.

-

Istisna’a (manufacturing)

This is a contract to acquire goods on behalf of a third party where the price is paid to the manufacturer in advance and the goods produced and delivered at a later date.

-

Ijarah and Ijara Wa Iqtina (leasing)

Under this mode, the banks buy the equipment or machinery and lease it out to their clients who may opt to buy the items eventually, in which case the monthly payments will consist of two components, i.e. rental for the use of the equipment and installment towards the purchase price.

-

Qard Hasan (benevolent loans)

This is the zero return type of loan that the Holy Quran urges Muslims to make available to those who need them. The borrower is obliged to repay only the principal amount of the loan, but is permitted to add a margin at his own discretion.

Contributed by : Mohd Kamil Hadsrim Ibrahim

Further explanation.

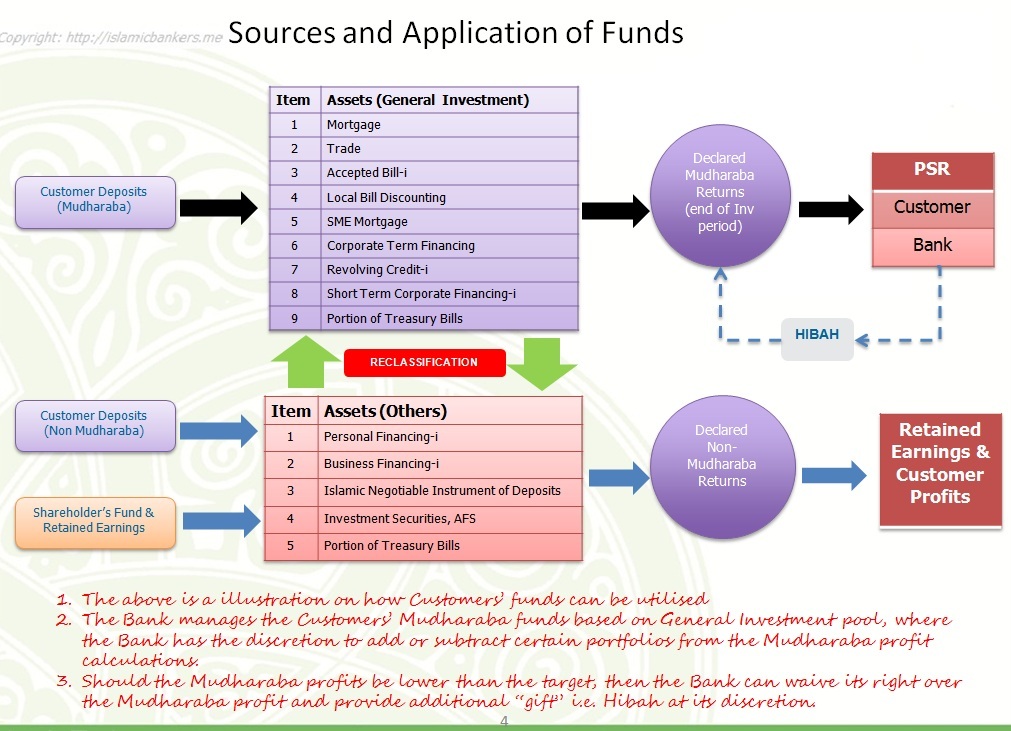

In general, the Balance Sheet of an Islamic Bank looks no different from a Conventional Bank. Conventionally, all deposits are managed internally and the Treasury team will use the funds as efficient as possible into the various instruments in the market. In this sense, all the deposits are used to fund mixed assets into a single pool, and its returns are a consolidation of all the returns derived from the assets.

Under the Islamic Banking regime, there is greater emphasis on matching the deposits against assets. While the management of the deposits into a single pool is not disallowed by Islamic Banking, it is the payment of returns that is most important under Sharia compliance where the fairness and justice to the customer is deemed to happen.

As such, to ensure that the returns to customer’s deposits (or investment) is fair, the level of transparency in the management of the deposits needs to be increased. Therefore, it is easier to be transparent when calculations are done based on “Funds”. In general, the funds are usually separated between “Mudharabah funds” and “Non-Mudharabah funds”.

There is specific guidelines on the treatment of Mudharabah funds (ROR Framework and Mudharabah Guidelines) as the Mudharabah arrangement is an investment contract between Bank and Customer. And since the contract has the risk element of potential capital losses arising from investments, it is important for the Bank to be transparent on the use of funds to the customers. More importantly, the IFSA recognised this that all Mudharabah-based deposit must be classified as an Investment, with its appropriate disclosures and risk warnings. It is prudent for the Bank to clearly separate the Mudharabah funds and match it against specific Assets where its “actual” performance can then justify the returns paid to depositors (investors).

With the introduction of the IFSA and the need to match Deposits into specific assets (as opposed to existing methods of investing into a “General” pool), Banks ideally must identify specific performing assets to enable clear calculation of returns back to the investors i.e. customers. Therefore, the amounf in the Pool of Deposit MUST BE equal to Pool f Assets where the Pool of Revenue is derived to pay a return to the Pool of Depositors.

Moving forward, under the IFSA and the issuance of the ROR Framework and new Investment Account guidelines, the sources and uses of funds become more important due to the elevated need of transparency and disclosure, as well as financial prudence of matching Assets against Liabilities.

Dear Mr. Amir,

I was reading through one of your pdf on Pool Management, so thanks for that…

The link for the same I have pasted below

Click to access pool-management-profit-calculation-distribution-mechanism.pdf

As usual I have a question ( few questions ), related to financing in Ijara and Ijara-Wa-Iqtina from the Investment Pool

1. Whenever there is a Financing done (in Ijarah / Ijarah-wa-iqtina) from the Deposit/Investment Pool, the asset will be owned by Bank initially, hence depreciation will come into picture.

Now when the rentals are received from the financing facility, this profit / rental has to be further distributed to the Pool deposit customers whose money was used for financing this facility. But as we know, on gross profit we need to deduct any direct expenses, depreciation, loss….on it. So the depreciation will be deducted from the Profit / Rental.

How is the principal recovered?, because the asset for leasing was purchased using depositors money kept in the pool, and at the end of the lease tenure the asset will be depreciated fully

2. As bank is required to pay the entire deposit capital (if no loss occur) to the Pool depositor, then from where the bank is now going to pay capital to it Pool customer? Leaving aside the profit portion (as that will be taken care by Rental received from Ijara finance).

Please correct me, if I am wrong on this, in Ijarah the (Principal + Rent) = Rent which is booked as a profit, which will further be distributed and attributed to each Pool depositor. So from where the bank is going to pay the Capital portion to the depositor on Mudarabah contract maturity?

Thanks for reading such a big question!! 🙂

Regards,

Prashant Vishwakarma

LikeLike

Hi Prashant,

Your questions are getting tougher hahaha but I know where you’re coming from.

Yes ideally if the funds originate from “investment account pool” based on the contract of Mudharabah, the funds can be used to invest into a “pure leasing” asset. Technically, once that happen, all the leasing returns (rentals) must flow back to the Mudharabah investors. It will be a flow through arrangement, where the investors hold the risks, records the lease asset in their books, and claim capital expenditure. This is pretty straight forward.

Your question presume that the Bank will use funds from Investment pool for Leasing activities. Truth is, we won’t due to the complexities you had also identified. Funds from investment pool either we use to finance debt, enter into mudharabah investment or place into interbank with islamic financial institutions.

More importantly, while you identified Ijara as one of the options for investment, hardly any Islamic Banks really do Ijara where it is an operating lease (ie ownership remains with the Bank and never transferred to customer). One of the Banks that I have worked in before had tried to do Ijara = operating lease (equity structure) where capital expenditure is a recovered expense, the NAV happens in the assets recorded in our balance sheet. At the end of the decision, the Bank reverted to AITAB where ownership is transferred thus making it a Financial Lease ie a debt structure. Therefore once it becomes debt, it behaves like any other types of financing.

And even if we do eventually go into a pure Ijara / Operational Lease structure, most likely the structure will be funded by the Bank’s funds rather than depositors funds, simply due to the capex considerations.

While a few banks have tried to look at really operationalising the Ijara structure, it is still unfortunate that the Banks are designed mostly for lending activities. Eventually one bank will make it work, but as you have pointed out, there are issues that the Banks are aware of but yet to be fully resolved.

Hope my long answer answers your question.

The short answer; we have yet to do Operating Lease.

Thanks Prashant

LikeLike

Hi Mr. Amir,

Thanks for bearing me for all these time…. hahahaha. Actually, very passionate to learn everything about Islamic Banking. I have posted some questions on other website too, but I never get a reply from them.

But you being such an experienced person into this vast industry, then also you take time to attend our naive questions like mine, is really commendable. Thanks for that..seriously!!

But I am still not clear how will Financial Ijarah not bear a capital Expenditure? Because we are any ways depreciating asset which will be charged to the Gross Profit (which will consist Principal + Rent) and again same condition arises as that of Operational Ijarah.

Thanks in advance 🙂

Regards,

Prashant Vishwakarma

LikeLike

No worries Prashant,

As much as you are asking me questions, I always learn new things as well. And I doubt you really are naive from the line of questions hahaha.

The depreciation issue and recording the asset as part of the bank’s balance sheet is applicable for operating lease type of product, ie pure Ijara where ownership never transfers to customer and therefore part of the bank’s total asset. It is not part of the financial asset line which you usually see listed as “loans and advances”. It is listed as Fixed Assets that generate “rental” income. Depreciation is allocated and deducted as part of the expense line. Rental is recorded in P&L as “Rental Income”. At the end of the lease period, there may be a secondary lease period, or the asset is eventually disposed to a third party at residual value. This is consistent with any conventional leasing arrangement.

But once there is a possibility of a leasing arrangement ending up with transfer of ownership, via last instalment sale, gift or ownership transfer, then it becomes a financial lease akin to Hire Purchase arrangement. It becomes a financing line, and you find the entries in the “loans and advances” line. Any depreciation is therefore not required to be calculated although it is called and “ijarah”, because it really is hire purchase. The income line is called “income from financing activities” instead of “rental income”. Therefore, this financing income can be parked under the pool of financing income, which may be distributable to customers under Mudharabah or Wadiah or Commodity Murabahah. This means, financial lease or hire purchase may be financed by depositors fund. There should not be any depreciation element in the bank books; if there is it has to be clawed back.

In the customers books, hire purchase depreciation resides there. It is their asset, their NAV, and ownership. And they would have a financial obligation line in their expenses, usually called “installments”.

For operating lease ie pure leasing, the assets do not reside in the customers books. They don’t claim the depreciation. Their fixed asset do not include the lease asset. There is only a “rental” payment in their P&L.

That is my understanding on the treatment of the products I have managed before. In general, banks shy away from operational lease, because it is administratively tedious.

I do stand corrected if this understabding is not consistent with what you see in financial statements. In truth, many banks call a product as “ijara” but many are essentially “hire purchase” instead. The financial statements reflects as such.

Hope we have the same views on this. Enjoyed your questions!

Amir

LikeLike

Thanks a ton Mr. Amir!!

Your last answer was very important and beneficial for my knowledge. Thanks again… So one thing understood, that in case of Financial Ijarah, bank will not book any expense under depreciation head…right? 🙂

But this one is last question on this topic… hahahaha…trust me 🙂

In Murabaha facility where Asset Cost and Markup both are separately shown (or recorded) in the financial statement, which implies that recovered ‘Asset cost’ will be used for paying the Pool Depositor’s capital on maturity and Markup will be used for paying the profit to them.

But in Financial Ijarah, the Asset Cost and Rent both are realized as income and will be shown under head ‘Income from financing activity’, so will the bank consider entire Income for distribution to Pool depositor’s? If yes, then from where the bank will pay the Pool Depositor’s capital deposit?

Thanks again 🙂

Regards,

Prashant Vishwakarma

LikeLike

Hi Prashant,

Financial Ijarah and Murabahah accounting treatment will both be the same treatment; both are debt financing.

Customers settle the Murabahah obligations via installments, which contains the principal and profit elements. The principal payment reduces the “financing receivables” and increases “cash” in balance sheet, and in P&L the profit becomes “income received from financing activities”.

Financial lease aka hire purchase works the same way as well. The Rental installment will consist of two elements as well ie Principal and Rental. Principal payments reduces the “lease receivables” in the Balance Sheet, as well as increasing “Cash” for the Asset cost (principal recovered). In the P&L, the rental portion becomes “income received from financing activities” as well.

It should not be recorded as “income received from leasing activities” as that will denote an operating lease rental proceeds. In operating lease, the Asset books gets reduced by depreciation amount (unless you do a market revaluation on the asset value), your “Cash” increases from the Rental proceeds which is the principal amount. In the P&L, the two lines affected is therefore the “Income from Leasing activities” or “Rental proceeds”, and the expense line where the “Depreciation” is showing.

Hope that clarifies my understanding on the structures. As mentioned, not many banks are equiped to operate “Leasing” activities. I started my working life in a Leasing/Hire Purchase company in 1997, and the administrative work that goes into a leasing company is significant. Even after the lease period we have to continue to revalue assets for secondary lease period, and keep track of all the assets and its conditions. Site visits are a must as these assets are the Bank’s Assets in the Balance Sheet. It is not just a financial obligation for the Bank, it really is a “rental of asset” arrangement to customers, where the leasing asset must be kept in good order for us to “earn the rent”.

Thanks for your questions, Prashant. No worries about asking more questions. If I can answer them, I generally do my best to answer it. If I do not know the right answer, I will probably give a vague answer or not respond!

Thanks

Amir

LikeLike

Thnks a ton..!! Mr. Amir. I now have a crystal clear understanding of Pool Management done for Operational Ijarah and Financial Ijarah.

Thnks again for helping me…!! 🙂

Regards,

Prashant Vishwakarma

LikeLike

Glad I can help, Prashant.

I will also answer your question on the rate of return for mudharabah soonest with illustration

Thanks

Amir

LikeLike

I am grateful Mr. Amir for your support and yes looking forward for your illustration. Please keep your support with us, where we (practical knowledge seekers) hardly get a chance to interact to a person like you. 🙂

Thanks again.

Regards,

Prashant Vishwakarma

LikeLike

Apologies Prashant, I haven’t finished with the illustration on Mudharabah and its calculation. Actually I am doing a dedicated post for this hopefully I will find that final time to complete this post. February InshaAllah

LikeLike

Dear Mr Amir, Thanks for sharing!!- Azmir

LikeLike

You’re welcome, Azmir

LikeLike

Sir, It is really helpful, Thanks

LikeLike

Pingback: What exactly do Islamic Banks do with the invested funds – Islamic Seeds